DMO Insights – July 14

In this edition:

- – LATEST RESEARCH FINDINGS FROM DESTINATION ANALYSTS

- – GROUPS: THE TIME TO BE SELLING IS NOW

- – KEY TAKEAWAYS FROM EXPEDIA’S 2020 SUMMER TRAVEL REPORT

- – WHAT HAPPENED TO ‘FLATTENING THE CURVE?’

- – RECENT NEWS & USEFUL LINKS

Where do we go from here? Back on June 8 we wrote that “More COVID-19 cases do not equal panic…yet” and while most states and destinations haven’t pulled the ripcord yet, they are at least holding it in their hand as the further tightening of restrictions, possible rollbacks into previous phases, and a slowing of reopening progress is already occurring.

These weekly DMO insights were never intended to look at travel through rose-colored glasses. Rather they are meant to help keep you informed and aware of the key impacts COVID-19 is having on tourism, and to present that information – the good, the bad, and sometimes even the ugly – in a manner that is quick, easy, and insightful.

Unless or until states take formal action to further restrict movement, people will continue to make individual decisions about travel based on factors including their personal beliefs and concerns, the situation in their own community vs. other communities, and an assessment of the risk/reward of staying at home vs. hitting the road.

Travel is an experience, and ‘experiences’ often trump ‘things’ when it comes to the happiness we derive from both. And who couldn’t use a little extra happiness in their life right now?

Thanks, as always, for reading, and we hope you continue to find value in this newsletter.

DESTINATION ANALYSTS’ WEEKLY SURVEY FINDINGS

There’s a mix of good and bad in this week’s survey findings from Destination Analysts. As the number of cases continues to rise, more than 41 percent of travelers now say they have no trip plans for the rest of the year. At the same time, 35.7 percent expect to be traveling by fall. Amid all the uncertainty, these numbers are extremely volatile and can (and likely will) continue to yo-yo from week to week.

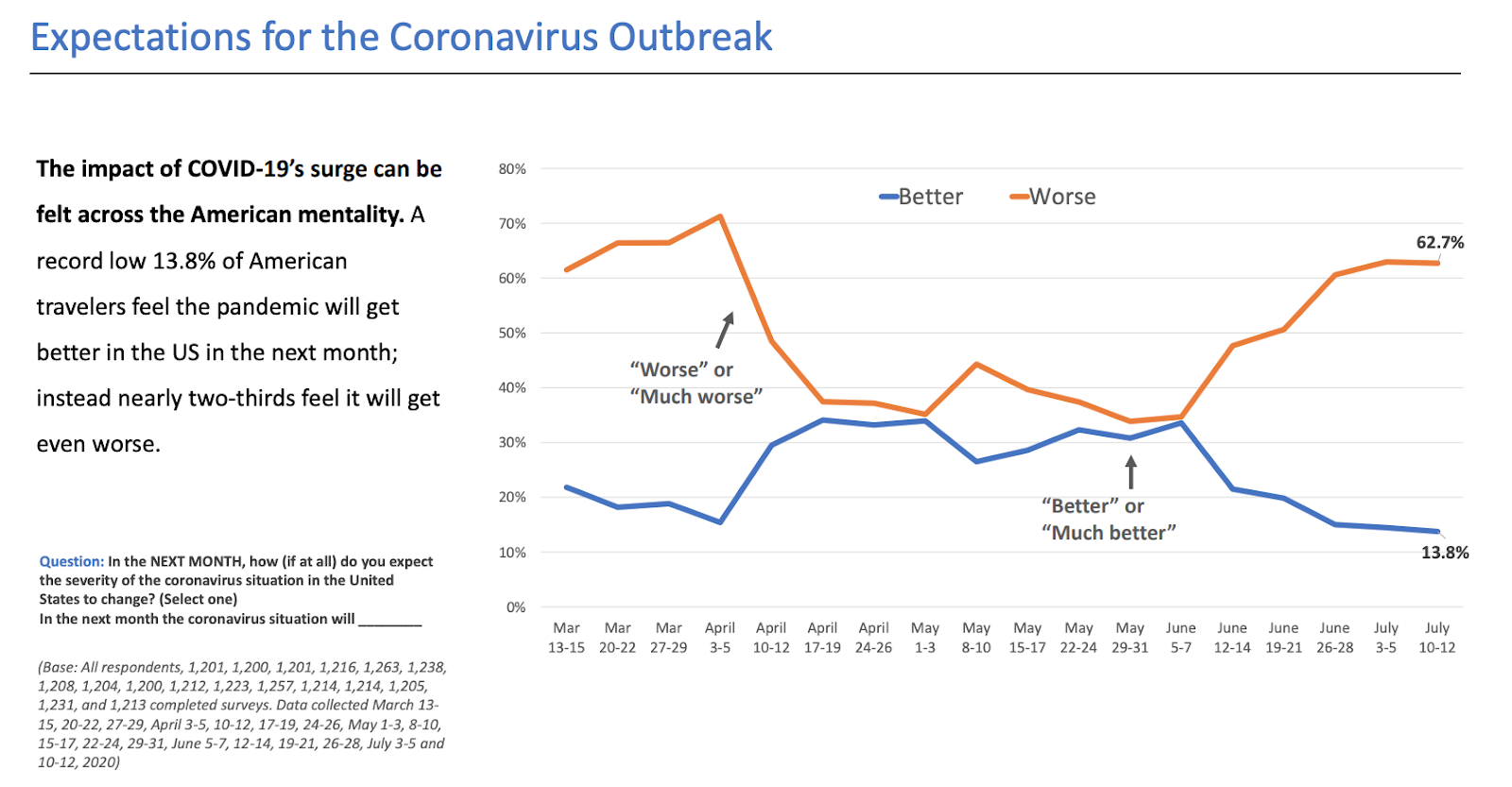

The optimism gap is officially a chasm: The chart says it all here. We are back to late March/early April numbers with regard to the number of travelers who believe the situation will get better or worse in the next month. The good news is that the gap only grew by 0.4% this week. The bad news? The numbers started heading in opposite directions about two weeks after Memorial Day weekend and the related physical distancing indiscretions, and we are still waiting to see what impacts July 4 weekend has on the number of cases.

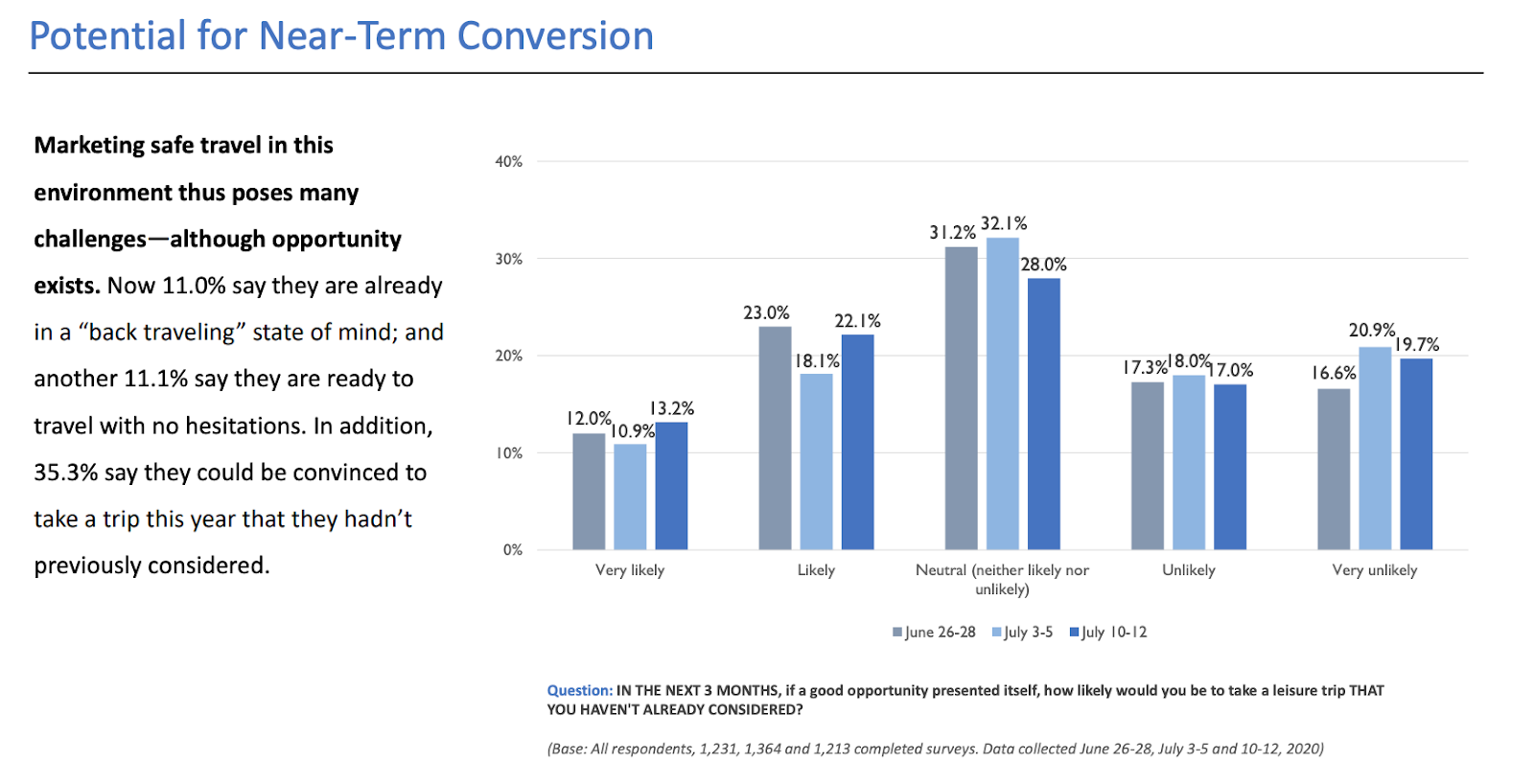

Short-term opportunities: Planning and booking windows are among the shortest they have ever been as most people take a ‘wait and see’ approach before making last-minute decisions about where to travel, or whether to travel at all. The number of travelers who are likely or very likely to take a trip in the next three months if the right opportunity presented itself stands at 35.3 percent, about the same as those who are unlikely or very unlikely to do so (36.7%). The actions of the middle ground – those who are neutral (28%) – will likely be determined by what takes place over the next month and their swing one way or the other will have a big impact on remaining summer travel volume.

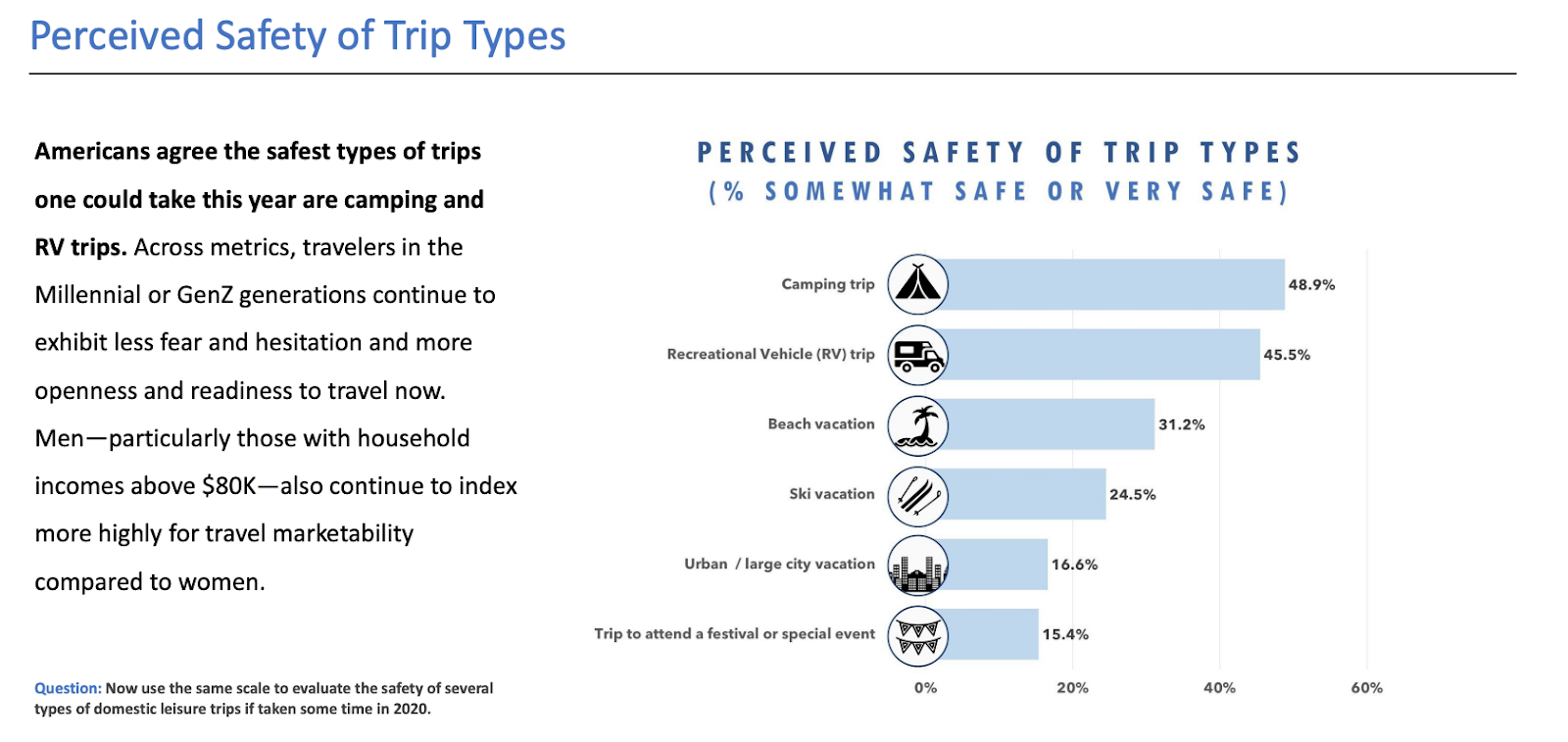

Getting away from it all – literally: Not surprisingly, camping and RV trips sit atop of the list of activities that travelers feel are safest right now. Three weeks ago we suggested that “destinations should start preparing for an influx of RV travelers”, and these numbers appear to support that claim. What’s surprising? Given the amount of negative publicity that beaches have received recently – largely due to Florida’s current outbreak – beach vacations still came in at #3 on the list.

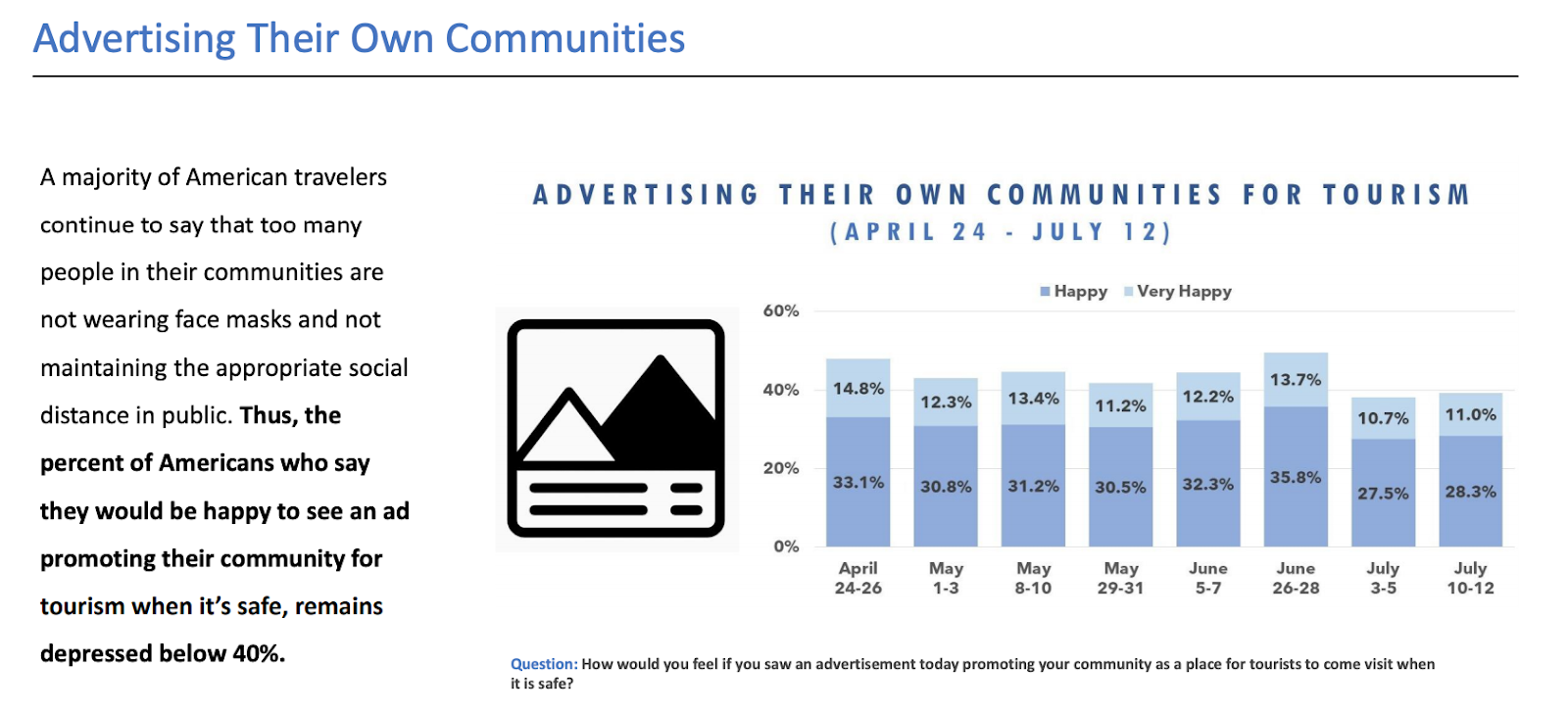

Local advertising sentiment remains low: Despite the importance of tourism to a community’s recovery, which we touch on in greater detail below, less than 40 percent said that seeing an ad encouraging people to visit their community when it is safe would make them feel happy or very happy. This further supports the need for ongoing messaging and education with regard to face coverings, physical distancing, and other personal safety precautions for both residents and visitors alike.

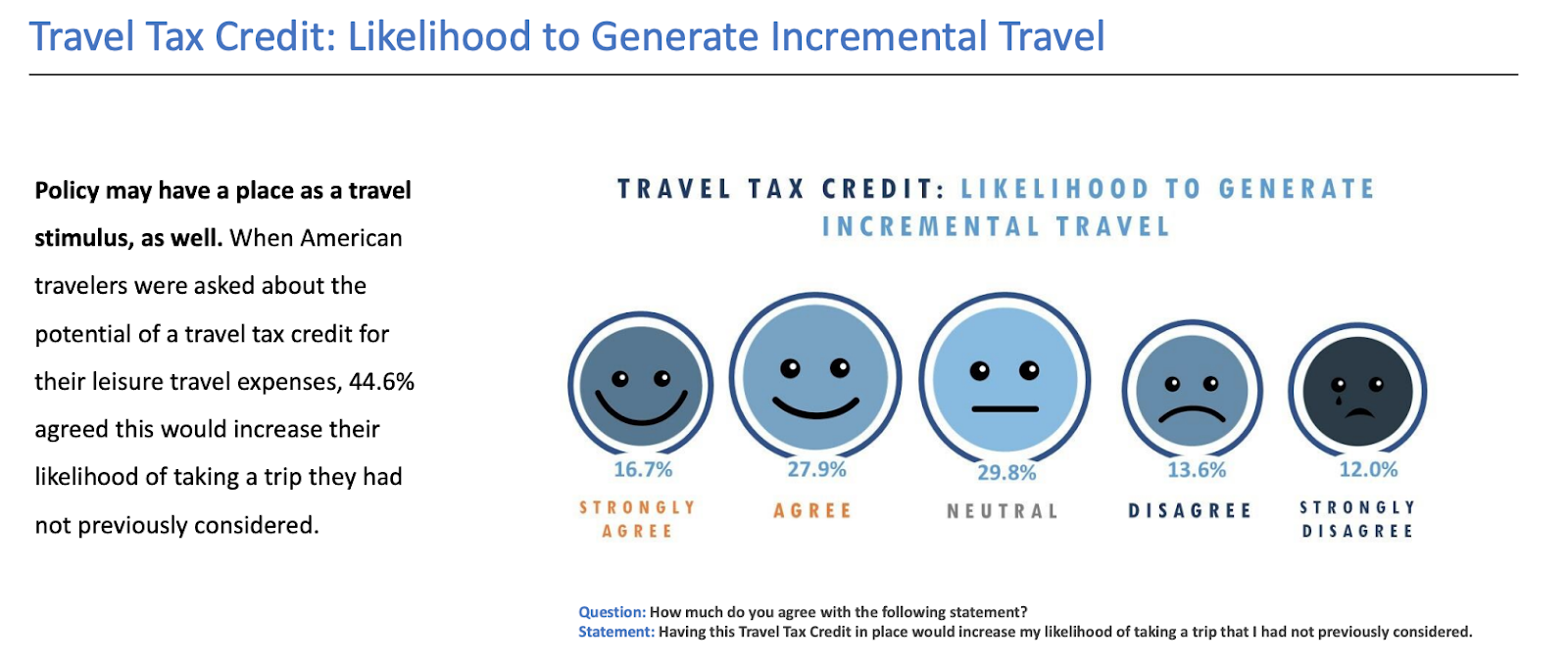

A travel tax credit might help: Although it is a long way from becoming reality, the proposed idea of a federal travel tax credit of $4,000 per American not surprisingly seems to have the support of travelers. Almost 45 percent of respondents indicated that the travel tax credit would increase their likelihood of taking a trip they had not previously considered.

GROUPS: NOW IS THE TIME TO BE SELLING

Will the meetings, conferences, and conventions industry rebound in 2021? The answer is most likely yes. And no. Or maybe, depending on who you ask.

While larger conferences and conventions such as the Consumer Electronics Show in Las Vegas face huge obstacles as outlined in this Forbes article titled “Will business travelers still flock to tradeshow and conventions despite COVID-19?”, there remains optimism that the industry – through a combination of downsizing, adapting to changing conditions, and evolving to meet shifting demand – is already recovering as demand increases for 2021.

If COVID-19 has taught us anything (it has taught us many things) about the way the economy functions, it is that with some exceptions it’s possible and even productive to conduct business in a remote or virtual environment. That being said, while group events are on hold for the time being there still exists a need and a desire for them to take place as soon as it is safe and acceptable to do so.

If your destination is not already planning, selling, and booking group business for 2021, it’s not too late but it’s definitely time to start doing so.

Yes, there is uncertainty and there are still a lot of things that need to take place before the group sales industry rebounds from COVID-19. Permission for large gatherings, expansion of currently reduced airline schedules, major overhauls to conference and convention venue operations, corporate permission to travel and attend large gatherings, and individual comfort with business travel are just a few of them.

But if history is any indication, those cards will fall into place over the remainder of 2020 and a new model for group meetings, conferences, and conventions will emerge. While that model will likely be different for large cities and those with massive investments in convention infrastructure, smaller second- or third-tier destinations are well-positioned to reap the benefits.

A few things to keep in mind when selling your destination in the current (and foreseeable) climate:

1. Smaller is better: Large scale conventions and conferences are unlikely to return to their pre-COVID levels in 2021. Not only does smaller (likely >50 people but potentially >100) apply to the size of meetings that should be targeted through sales efforts, it also applies to the smaller markets and destinations that are likely to be more appealing to meeting planners.

2. Think regional: Organizations and industries that have traditionally held a single annual conference or convention will be more likely to parse them into regional events in the interest of keeping group size smaller and manageable.

3. Go back to the well: Events that have historically rotated from one destination to another from year to year will be more likely to return to one they are familiar with. In reaching out to past clients, chances are you will find that they are more receptive to the idea and more interested in returning than you thought they might be.

4. Lead with your trump card: Smaller communities. Outdoor recreation. Within driving distance (>8 hours). Open spaces and venues. Committed to visitor health and safety. These are just a few of the trends that will continue to be prevalent in 2021. If any (or all) of them apply to your destination, then, by all means, tout them.

5. Demonstrate flexibility: Nobody is going to want to attend indoor meetings and work sessions all day, or stroll the aisles of a convention hall for hours on end, only to attend indoor cocktail receptions and dinners in the evening. Mixing in some outdoor or alternative meeting, activity, and social options, while always important to hosting a successful event, will be more important in 2021. They also give venues a chance to “turn over” (air circulation, cleaning, etc.) meeting spaces at various times throughout the day.

6. Invest in technology: For those who are uncomfortable with travel or are not allowed to travel, having the technology assets to pull off a hybrid in-person/virtual event could mean the difference between winning business and losing it. Virtual attendance can still be monetized to the benefit of the destination, allowing it to capture some of that revenue while still providing overall cost savings to the attendee or employer.

KEY TAKEAWAYS FROM EXPEDIA’S 2020 SUMMER TRAVEL REPORT

As the world’s largest online travel agency, Expedia should know a thing or two about forecasting trends and demand for leisure travel. In their recent 2020 Summer Travel Report, which included mining their own search and demand data as well as polling more than 1,000 Americans, Expedia was able to draw numerous conclusions. Among them were increased interest in same-state stays, road trips, and flexible travel plans.

While that’s not breaking news, perhaps the most notable finding in their report was this fact:

85 percent of U.S. travelers are planning or likely to take a road trip this summer.

That’s a huge number, and one that should create a sense of optimism among DMOs near and far. Adding to that news, year-over-year interest in summer domestic stays is up 10 percent, accounting for nearly 85 percent of hotel searches in June. Again, not surprising given the restrictions and uncertainty surrounding international travel, but good news nonetheless.

A few other notable highlights from the report, a summary of which is available at the link above, include:

1. Demand for staycations is on the rise: Nearly 85 percent of hotel searches on the site in June were for accommodations located within the U.S., and almost a quarter of June bookings were for same-state stays.

2. Last-minute getaways: More travelers are booking trips 0-7 days out this summer than in previous years according to the report, another indication that forecasting travel will be difficult with changing restrictions and consumer uncertainty and hesitation.

3. Flexibility is important: 97 percent of stays booked in June were refundable rates – a 20 percent increase year-over-year

4. Staying safe: Health, safety, and the avoidance of crowds are being prioritized over price point when it comes to travel. 72 percent of survey respondents said they’re opting for a road trip this summer because it feels safer than flying, and more people listed health and safety (72%) and avoiding crowds (68%) as top concerns over budget (60%).In fact, some travelers are even using price point as a means to avoid crowds by opting for privacy and exclusivity.

5. Fresh air & a change of scenery: Among the 85 percent of survey respondents who said they are planning or likely to take a road trip this summer, a change of scenery (43%) and the desire to enjoy the outdoors (36%) were among the top motivations mentioned.

6. Be prepared: Survey respondents suggested having a detailed travel plan (and a backup plan), knowing where to stay, doing vehicle maintenance, downloading apps, carrying cash, and packing the essentials including extra masks, food, water, toilet paper, sanitizer, and disinfecting wipes.

Data for the report was based on interest or demand on Expedia.com during June 2020 for travel between June 1 and September 7, 2020, compared to the same time periods in 2019. The consumer survey was commissioned by Expedia and conducted by Survey Monkey, polling 1,077 respondents, aged 18+, located in the U.S.

WHAT HAPPENED TO ‘FLATTENING THE CURVE?’

When it comes to our own safety and the safety of our families, we have said all along that we would rather be too cautious and look back thinking we could have been less careful, than be less careful and look back wishing we had been more cautious.

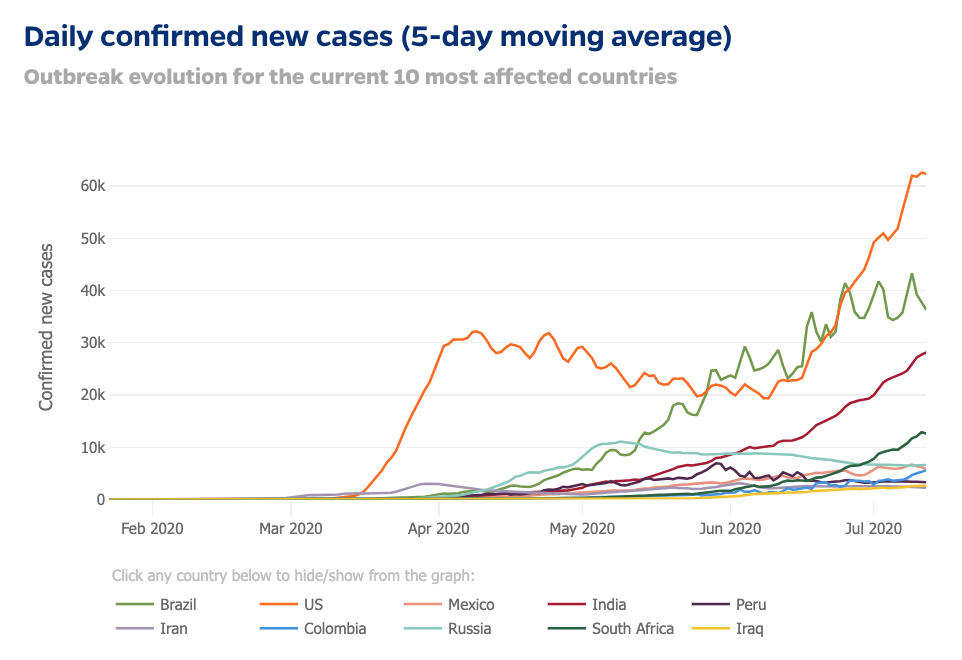

It’s the old “an ounce of prevention is worth a pound of cure” adage, and unfortunately, many states, counties, and individuals are learning that lesson the hard way right now while the number of new COVID-19 cases in the U.S. skyrockets as seen in the chart below.

So, what happened? How did flattening the curve work, and then break, and what can be done to fix it?

Well, flattening the curve worked for obvious reasons. We shut down. We stayed at home. We watched, and we waited. That patience, and those sacrifices, were evident in the number of new cases, which spiked in early April before starting to slowly taper. Pat yourself on the back. Give yourself a socially distant high five. And reward yourself by getting together with 10 of your closest friends to celebrate at a nearby bar.

Which is exactly what leads us to what broke.

We grew weary, tired, frustrated, caged. And the minute the first restrictions were lifted, it felt as though we had all been paroled. Gatherings were held. Face coverings were not worn. Life resumed. And many of us – despite strong warnings to the contrary from health officials – declared ourselves ‘winners’ in the fight against COVID-19.

Shortly afterward came Memorial Day Weekend, which should have been (and was, for many) an early indication that things were about to get worse, not better. The number of confirmed new cases started rising sharply in mid-June, which not coincidentally came as expected about two weeks after Memorial Day. They have continued rising steadily ever since, with record numbers being reported in many states and as a country overall while the toll from Fourth of July Weekend remains to be seen. Look for those numbers to start showing up around July 20.

Until then, here we are with more than 3 million documented cases of COVID-19 in our rearview mirror. To put that number into perspective, it took just over three months for the U.S. to reach 1 million cases on April 28. It took about half that time, 44 days, to get to 2 million cases on June 11. And it took only 26 days to reach 3 million cases on July 8. At that rate, we could very well reach 4 million cases as soon as July 22. Over that time, the average age of COVID-19 patients has dropped by 15 years, a further indication that the individuals who tend to be least compliant are also becoming the biggest spreaders, even if unknowingly at the time.

And if we could go back we would probably do things differently. Or maybe we wouldn’t. Here are a few of the things we may have done differently if given the opportunity today:

1. Allowing individual states to govern their own pandemic-related mandates, closures, orders, restrictions, and reopening processes.

2. Not implementing a national face covering mandate particularly after it became clear that, as reported in The Washington Post on June 5, “social distancing is over.”

3. Beginning to reopen the country prior to two major holiday weekends, Memorial Day and Fourth of July.

Hindsight is 20/20, but what we can do, and what we are seeing now, are states taking aggressive steps to counter the increase by mandating the use of face coverings indoors and outdoors, reducing gathering sizes, closing indoor dining and bars, and on the verge of returning to even stronger sanctions. It’s a bit of closing the barn door after the horses are out, but in a society where it seems to be easier to throw resources at a problem rather than change the behavior that is causing it, it’s a step in the right direction while we hobble along waiting for the silver bullet in the form of a vaccine.

RECENT NEWS & USEFUL LINKS

Recent News

The travel industry is turning to private jets to spark its recovery – Forbes – July 8

After months of telling people to stay away, some big cities need new ways to bring tourists back – NBC News – July 9

Bike Touring may be the perfect way to travel this summer – Treehugger – July 13

Marriott CEO on the future of the hospitality industry – Forbes – July 13

Best guess on when business travel will recover? It could be years – NY Times – July 13

Useful Links

Key Survey Findings – Week of July 12 – Destination Analysts

Expedia 2020 Summer Travel Report – Expedia, July 8

AirDNA Covid-19 Data Center – AirDNA – ongoing

Guidance for promoting the health & safety of all travelers – U.S. Travel